Year End Planning

Medicare can’t be avoided. Prepare yourself for the changes now…

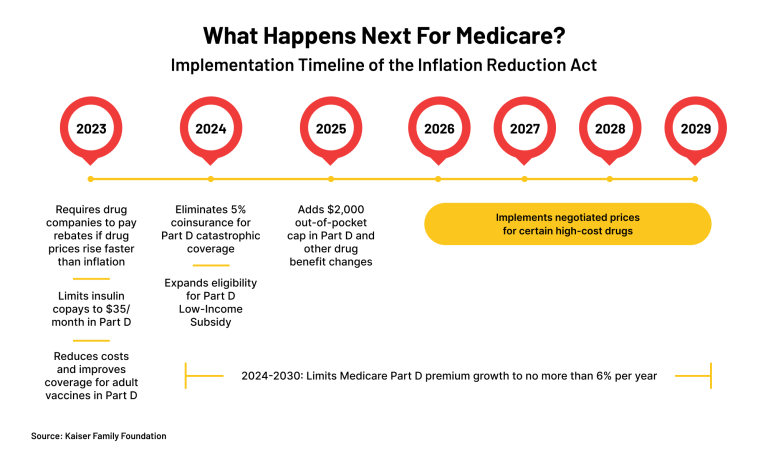

What happens next for Medicare?

New laws are here!

The new Inflation Reduction Act is a big piece of legislation. It is filled with green energy spending, corporate taxes and significant changes to Medicare.

⇒ Is this a big deal? Could be…

First here are some Medicare changes:

Medicare will be able to negotiate drug prices

Beginning in 2026, the Medicare program will be allowed for the first time ever to negotiate the cost of drugs. Before the negotiations begin, new rules will also require manufacturers to pay ‘rebates’ to the government if they increase covered drug prices higher than general inflation (’23) AND limit Medicare Part D increases each year (’24).

Why does this matter?

Drug price inflation is high. Thousands of medications are outpacing general inflation. The ability to negotiate prices should start to fix that. Medicaid has the ability to negotiate currently AND they are paying about 30% less for the same drugs.

Lower prices could lead to more savings passed on to you. We may even see a time when premiums get reduced.

Part D capped at $2,000 per year

Under current laws, there’s no cap on how much people have to spend out-of-pocket for their medications, which can really add up under cost-sharing requirements. Even to the extent I have seen it ruin some families financially.

> Starting in 2024, folks who spend enough out-of-pocket on medications to surpass the “catastrophic threshold” will no longer have to pay coinsurance for their expensive drugs.1

And, starting in 2025, the maximum out-of-pocket medicine cost for folks on Part D will be a flat $2,000.

Why does this matter?

Many drugs (especially new ones or ‘brand’ name) can be punishingly expensive. Capping these costs will insure a quaility of life folks deserve. It will also provide predictability to the costs… FINALLY.

Insulin costs will be capped at $35 monthly

Beginning in 2023, enrollees won’t have to spend more than $35 per month on insulin. On average, this cost is north of $500 annually. Much more expensive if you need a specific type. Capping costs could help the MILLIONS of people who need this LIFE SAVING medication.

All vaccines will be free under Part D (starting in 2023)

Believe it or not, not all vaccines are covered under Medicare Part D. Including shingles!

Will these laws help retirees?

This is where the future gets hazy. Legal challenges or post-election changes could end up altering much of what’s in the Inflation Reduction Act.

> And much depends on the actual execution of the new rules.

The new rules could also mean premium changes as insurance companies figure out their models.

Since health care is one of the biggest unknown costs in retirement, lowering drug costs and making spending more predictable for Medicare recipients could absolutely have a positive impact on millions of people. I believe it offers momentum toward a more simple system.

Is the Inflation Reduction Act a 'Good' move for the economy?

Whether the overall bill will live up to its name, lower inflation, and have a net positive impact on the economy also remains to be seen.

Some economists project that the bill will end up modestly reducing inflation and trimming the federal budget over the next decade.5

> I am not an economist so I believe someone is going to pay for the changes… this can not realistically trim our debt.

Others are concerned about the impact of the new corporate tax rules written into the legislation.

As is usually the case, time will tell. There is a line forming at the courthouse…

Resources

I need the basics!

Use this guide to better understand the basics of Medicare.Use this guide to better understand the basics of Medicare.

Will I avoid Medicare enrollment penalties?

If Medicare enrollment rules are not followed correctly, you may be subject to significant penalties. It is important to understand available options, applicable deadlines, and your unique circumstances in order to properly enroll in Medicare and avoid penalties.

To help make this analysis easier, we have created the Will-I-Avoid-Medicare-Enrollment-Penalties-2022 flowchart. It addresses some of the most common issues that clients face, including:

- Impact of employee headcount for those covered under an employer plan

- Special Enrollment Period rules

- Penalties for delaying Part A, B, & D

- How a creditable drug plan could impact Part D late enrollment penalties

Will I avoid IRMAA surcharges on Medicare Part B & Part D?

Planning around Income-Related Monthly Adjustment Amount (“IRMAA”) surcharges has become more important as the Medicare premium increase amount has grown in recent years. While on the surface the concept is pretty straightforward, there are a few issues that can cause an unexpected wrinkle for you. It can be difficult to avoid pitfalls, and to recognize when you may be able to request an exception from the IRMAA surcharge.

To help make this easier, please use the resource “Will I avoid IRMAA Medicare surges?” flowchart. It addresses some of the most common issues that arise for a client on Medicare, including:

- IRMAA surcharges for Part B and Part D based on MAGI ranges

- Situations to request an exception and the form to complete

- Relevant tax year for the surcharge calculation

Will I be automatically enrolled in Medicare?

Determining when to enroll in Medicare can be complicated. Depending on the your situation, you may be automatically enrolled or you may have to proactively enroll.

If you must follow the Initial Enrollment Period rules, there is the added complication of determining when coverage starts.

To help make this analysis easier, we have created the ‘Will I be automatically enrolled?” flowchart. It addresses some of the most common Medicare issues that arise when a client turns 65, including:

- Impact of age on enrollment

- Automatic enrollment events

- Initial Enrollment Period rules

- Coverage start dates for Part A, B, & D

Should I change my Medicare coverage during open enrollment?

Many folks currently rely on Medicare plans for their health care coverage. They may have enrolled in Original Medicare or Medicare Advantage, and they likely have prescription drug coverage as well. For current beneficiaries of all of these plans (Medicare A, B, C, and D), October 15 marks the beginning of the Open Enrollment Period, during which changes in coverage may be made.

This flowchart helps guide you through a series of considerations when evaluating and comparing their Medicare options. It covers:

- Changes in health care needs

- Costs of premiums, deductibles, etc.

- Access to specific providers, services, and prescription drugs

- Out-of-state concerns

- Effective dates of any changes